The Intelligence Layer

How Precision Agriculture Is Transforming Golf Course Management

Key Takeaways:

At 5:30 a.m., a superintendent walks a fairway in the half-light before dawn. He stops, kneels, and presses his hand into the turf. Too wet here. Dry over there. He makes a mental note, moves on. By the time the first group tees off, he will have made dozens of decisions based on feel, experience, and a handful of spot measurements.

This scene has played out on golf courses for a century. It is about to change.

The same forces that transformed row-crop agriculture over the past two decades—precision sensing, data integration, and automated decision-making—are now arriving in golf. The implications for course operations, capital allocation, and investment are substantial. And the transition is happening faster than most operators realize.

The Macro Thesis: Why Precision Agronomy Is Inevitable

Five structural forces are converging to reshape how golf courses must be managed:

Water scarcity. California, Arizona, and Southwest markets face mounting restrictions. Golf courses are among the highest water consumers in the sports and leisure industry, with many using millions of gallons annually. Water is no longer cheap or unlimited—and regulations are tightening.

Labor constraints. Superintendent staffing is at historic lows. The burden of synthesizing fragmented data—soil conditions, weather, equipment schedules, agronomic practices—falls on humans already stretched thin. Decision-support tools are no longer optional.

Rising input costs. Fertilizers, wetting agents, pesticides, and energy have all increased in price. Uniform application across an entire course—regardless of actual conditions—is becoming economically irrational.

Playing condition expectations. Tour-level standards are filtering down to daily-fee courses. Golfers expect firm-and-fast conditions, and superintendents need tools to deliver them consistently—not just on tournament days, but every day.

ESG and sustainability reporting. Private equity and institutional owners increasingly require water and chemical use documentation. Data is becoming a compliance requirement, not a luxury.

These forces don't ask permission. They compress operating margins, shorten decision windows, and favor courses that can respond with precision. The transition to data-driven agronomy is not a matter of if—it's a matter of when and how fast.

The Agricultural Precedent: What Row-Crop Farming Figured Out

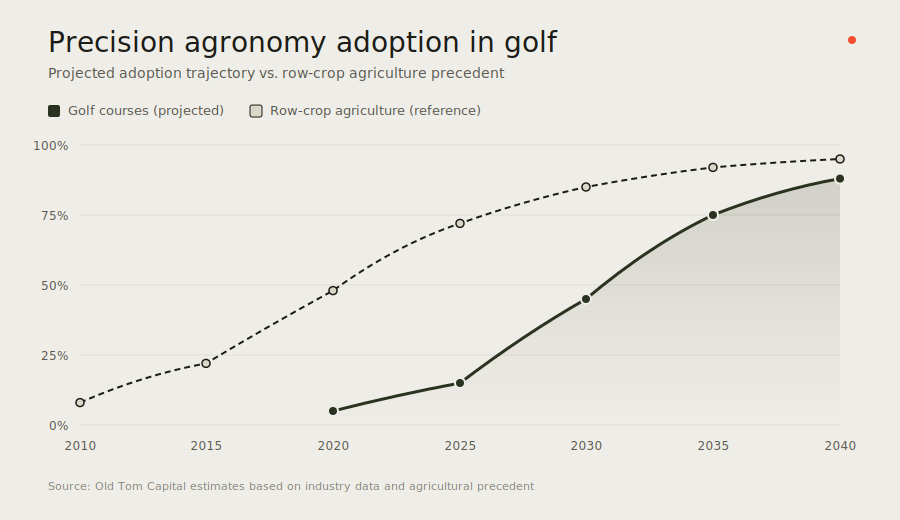

Golf is roughly a decade behind precision agriculture in its adoption of data-driven management. That gap is instructive—because agriculture has already demonstrated what works.

The transformation began in the 1990s with GPS-guided tractors and yield mapping. By the 2000s, variable-rate application systems allowed farmers to adjust fertilizer and pesticide rates in real time based on sensor data. The 2010s brought sensor networks, satellite imagery, and IoT integration. Today, artificial intelligence and autonomous equipment are closing the loop between sensing and action.

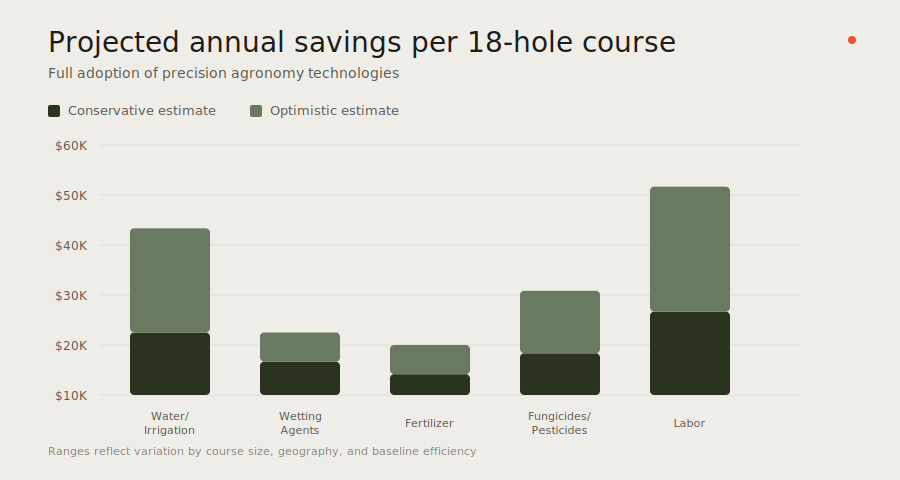

The economics are compelling. Variable-rate application systems routinely deliver 10–30% reductions in chemical and fertilizer inputs while maintaining or improving yields. Precision irrigation reduces water use by 20–30% in many deployments. The return on investment is measurable and repeatable.

But the deeper lesson is about where value accrues.

Equipment manufacturers recognized that hardware was commoditizing. They began acquiring the intelligence layer—the companies that control data and decision engines. John Deere acquired Blue River Technology. CNH acquired Raven Industries. Valmont acquired Prospera. The pattern was clear: own the brains, not just the machinery.

Golf is following the same path. The winners will not be companies selling sensors in isolation—they will be companies that translate sensing data into prescriptions and automated action. Hardware becomes the delivery mechanism for intelligence.

Translation to Turf: The Emerging Stack

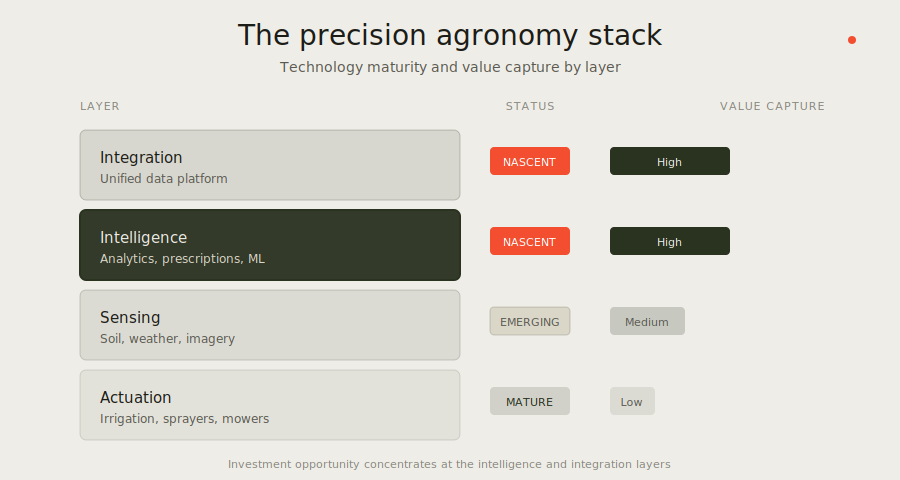

The traditional golf course operating model is reactive. A superintendent observes conditions, makes a judgment call, applies inputs uniformly, and adjusts when problems emerge. It works—but it depends entirely on human bandwidth and accumulated intuition.

The precision agronomy model is different. It begins with continuous sensing—soil moisture, weather, plant health—feeding into a unified data platform. Analytics generate zone-based prescriptions. Automated systems execute. And outcomes are measured, creating a feedback loop that improves over time.

Several layers of this stack are emerging in golf. Sensing technologies are advancing rapidly. Actuation—irrigation systems, sprayers, mowers—already exists and is increasingly connected. But the intelligence layer in the middle remains nascent. No dominant platform yet integrates sensing, analysis, and execution into a unified operating system for turf management.

This is where value will accrue.

Data-Driven Agronomy in Practice

The shift is already underway, driven by organizations willing to experiment and quantify results.

Shot Data and Turf Reduction

The USGA Green Section—long a leader in agronomic research and course consulting—recently published work that illustrates the power of data-driven decision making. In collaboration with Arccos, they are using shot location data to help courses identify opportunities for turf reduction.

The premise is simple but powerful: many golf courses maintain significant acreage of irrigated, regularly mown turf that experiences very little play. These areas consume water, labor, and inputs—but contribute almost nothing to the playing experience.

By mapping shot data from hundreds of golfers across thousands of rounds, the Green Section can visualize exactly where play concentrates—and where it doesn't. The patterns are immediately apparent. Courses can then outline potential turf reduction areas based on objective criteria, such as removing maintained turf that affects no more than 5% of tee-to-green shots.

As the Green Section notes: "Having a more objective and accurate understanding of how play is distributed across a golf course makes it much easier to identify areas for turf reduction that offer the most benefits with the least impact on play."

This is yield mapping for golf—using outcome data to inform resource allocation. The full article is available at the USGA Green Section Record:

Precision Irrigation

Soil moisture sensing represents another frontier. Traditional methods rely on handheld probes that provide point measurements—useful, but labor-intensive and spatially limited. A superintendent might take a dozen readings across a fairway and extrapolate. The gaps are filled by intuition.

Emerging sensing technologies deliver thousands of measurements per pass, creating high-resolution maps of moisture variability at the root zone. This shifts irrigation from schedule-based to condition-based. Water goes only where it's needed—and just as importantly, doesn't go where it isn't.

The counterintuitive insight is that better playing conditions and water conservation are not trade-offs—they're complements. Firm-and-fast turf requires precision, not excess water. Courses that adopt precision irrigation often report 20–30% reductions in water use while improving playability.

Variable-Rate Application

The next frontier is zone-based chemical application. Wetting agents, fungicides, and fertilizers are typically applied uniformly—even though conditions vary dramatically across a single fairway. GPS-enabled sprayers can now apply inputs at variable rates based on prescription maps generated from sensing data.

Early implementations suggest the potential for substantial reductions in chemical use—in some cases exceeding 50%—with maintained or improved turf quality. The economics are compelling: fewer inputs, less labor, better outcomes.

Case Study: TerraRad

Old Tom Capital invested significantly in TerraRad, a company at the forefront of precision soil moisture sensing for turf. The investment exemplifies our thesis on where value accrues in the emerging agronomy stack.

TerraRad's core technology—a patented passive microwave sensor—measures root-zone soil moisture with precision and scale that existing tools cannot match. Unlike handheld probes that require manual labor and produce sparse data, or satellite imagery that cannot penetrate to the root zone, TerraRad delivers continuous, spatially resolved moisture intelligence.

Our investment thesis centered on three convictions:

First, water is becoming the binding constraint for golf course operations in many markets. Tools that enable courses to do more with less are not discretionary—they are essential.

Second, the traditional agronomy tools available to superintendents—visual inspection, manual probing, intuition—are inadequate for the precision that modern conditions demand. There is a genuine technology gap waiting to be filled.

Third, value in precision agronomy migrates toward the intelligence layer. TerraRad is building not just a sensor, but a platform that transforms sensing data into actionable decisions—prescription maps, integration with irrigation systems, and analytics that improve over time.

The company has already validated its technology at the highest levels of the sport, working with PGA TOUR agronomy teams and top-ranked courses. Its exclusive integration partnership with the dominant U.S. golf irrigation provider opens distribution to thousands of courses.

TerraRad also demonstrates the platform extensibility that makes precision sensing companies strategically valuable. The same core technology applies to adjacent markets—forage crops, orchards, construction—where moisture management is equally critical. This optionality expands the total addressable opportunity far beyond golf alone.

The Investment Landscape

Golf offers an attractive market for precision agronomy technology. Courses maintain higher margins per acre than row crops and have aesthetic and performance standards that create willingness to pay. The customer base is captive—more than 16,000 courses in the United States alone—and equipment replacement cycles create natural upgrade windows.

Yet the market remains underpenetrated. Industry data shows that 2024 was the first year more than half of superintendents reported using handheld soil moisture sensors—up from just 33% in 2013. Formal irrigation scheduling programs crossed the 50% threshold the same year. The adoption curve is steepening, but significant runway remains.

The strategic opportunity lies in the fragmentation of today's market. Sensing exists. Actuation exists. But the unifying platform that translates data into decisions—the intelligence layer—is nascent. Companies that establish this layer will capture disproportionate value as the market matures.

The exit path is well-established. Equipment OEMs have demonstrated willingness to acquire intelligence-layer companies at strategic premiums. The pattern from row-crop agriculture—where Deere, CNH, and Valmont paid hundreds of millions for sensing and software platforms—will likely repeat in golf. The dominant equipment and irrigation providers cannot afford to be dependent on platforms they do not control.

The Road Ahead: A Ten-Year View

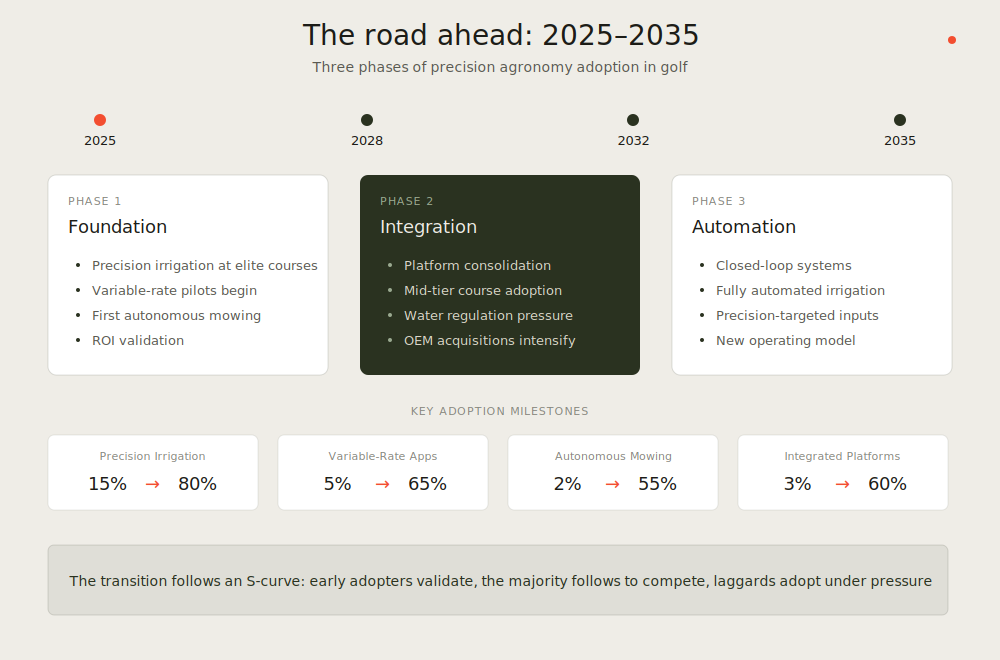

Precision agronomy will not arrive uniformly. The transition will unfold in three distinct phases, each building on the last. Understanding this trajectory is essential for operators planning capital investments and investors evaluating opportunities.

Phase 1: Foundation (2025–2028)

The next three years will establish the foundational technologies. Precision irrigation will become standard practice at elite courses—Top 100 private clubs, Tour venues, and high-end resorts. These early adopters will validate ROI, refine workflows, and create peer pressure for the next tier.

Variable-rate chemical application will move from pilot programs to early commercial deployment. Superintendents who have struggled with wetting agent costs and uneven results will begin generating GPS-based prescription maps from moisture data. The economics will prove out: 40–60% reductions in chemical inputs with improved uniformity.

Autonomous mowing will see its first meaningful deployments on fairways and roughs. Labor savings will drive adoption, but the more significant development will be the data these machines generate—coverage maps, terrain modeling, and integration points for broader course intelligence.

By 2028, the question at industry conferences will shift from "Should we adopt precision tools?" to "Which platforms are winning?"

Phase 2: Integration (2028–2032)

The middle phase will be defined by platform consolidation. Standalone sensing tools will give way to integrated systems that connect moisture data, weather feeds, irrigation controllers, and application equipment. The winners will be companies that own the integration layer—the operating system that coordinates disparate tools into coherent action.

Mid-tier courses—upper-end daily fee, mid-range private clubs—will adopt precision tools as costs decline and the technology matures. Adoption will be driven less by innovation appetite than by competitive necessity. Courses that achieve better conditions at lower cost will attract members and rounds; those that don't will struggle.

Water regulations will accelerate the transition. California, Arizona, Nevada, and other water-stressed markets will tighten allocations. Courses will need to demonstrate—with data—that they are using water efficiently. Precision irrigation will shift from a competitive advantage to a regulatory requirement.

OEM consolidation will intensify. Equipment and irrigation manufacturers will acquire sensing and software platforms to control the intelligence layer. The acquisition pattern from row-crop agriculture will repeat in golf—likely at premium valuations as strategic buyers compete for scarce assets.

Phase 3: Automation (2032–2035)

The final phase will close the loop. Sensing, decision-making, and execution will operate as a unified system with minimal human intervention. The superintendent's role will evolve from data gatherer and decision-maker to system supervisor and exception handler.

Irrigation will be fully automated—not on timers, but on real-time soil conditions. Sprinklers will activate based on root-zone moisture thresholds, adjusted for weather forecasts, and optimized across the entire course as a system. Water use will decline another 15–20% from already-improved baselines.

Chemical application will be precision-targeted. Disease and pest pressure will be detected early through imagery and sensor fusion, with treatments applied only where needed. The era of calendar-based preventive spraying will end. Input costs will fall; environmental footprints will shrink; turf health will improve.

Autonomous equipment will handle the majority of mowing, with human operators focusing on detail work and oversight. The labor model will shift from large crews performing repetitive tasks to smaller teams managing automated systems.

By 2035, precision agronomy will be the default operating model. Manual-only operations will be the exception—found primarily at courses that cannot or will not invest in modern infrastructure. The competitive gap between data-driven courses and traditional operations will be too wide to ignore.

The Investment Landscape

Golf offers an attractive market for precision agronomy technology. Courses maintain higher margins per acre than row crops and have aesthetic and performance standards that create willingness to pay. The customer base is captive—more than 16,000 courses in the United States alone—and equipment replacement cycles create natural upgrade windows.

Yet the market remains underpenetrated. Industry data shows that 2024 was the first year more than half of superintendents reported using handheld soil moisture sensors—up from just 33% in 2013. Formal irrigation scheduling programs crossed the 50% threshold the same year. The adoption curve is steepening, but significant runway remains.

The strategic opportunity lies in the fragmentation of today's market. Sensing exists. Actuation exists. But the unifying platform that translates data into decisions—the intelligence layer—is nascent. Companies that establish this layer will capture disproportionate value as the market matures.

The exit path is well-established. Equipment OEMs have demonstrated willingness to acquire intelligence-layer companies at strategic premiums. The pattern from row-crop agriculture—where Deere, CNH, and Valmont paid hundreds of millions for sensing and software platforms—will likely repeat in golf. The dominant equipment and irrigation providers cannot afford to be dependent on platforms they do not control.

Conclusion: The Inevitable Transition

The adoption curve will be an S-curve, not a linear ramp. Early adopters validate. The early majority follows to remain competitive. Laggards adopt when the alternative becomes untenable. Once the curve steepens, the transition happens faster than most expect.

For golf course operators, the strategic imperative is clear: precision agronomy is not a technology experiment—it is the future operating model. Courses that invest early in sensing, data integration, and automated decision-making will achieve better playing conditions at lower cost. Those that delay will find themselves at a competitive disadvantage that widens with each passing year.

For investors, the opportunity is equally clear. Golf is following the same path that transformed row-crop agriculture. The technologies are proven. The market is large and captive. The structural forces driving adoption are intensifying. And the exit paths are well-established.

Old Tom Capital is actively deploying into this space. We seek companies positioned at the intelligence layer—where sensing data is translated into prescriptions and automated action. We look for technologies with clear ROI for customers, strategic partnerships with dominant OEMs, and platform extensibility into adjacent markets.

The superintendent who walks the fairway at dawn will always bring judgment and craft to his work. But increasingly, he will be supported by tools that see what he cannot—continuous, precise, and everywhere at once. That is the intelligence layer. And it is coming to golf.